How to Integrate a Fiat On-Ramp Into Your Crypto Exchange 2026

Introduction

Your users show up with dollars. If converting them to crypto takes more than three clicks, those users leave — and they don’t come back. Learning how to integrate a fiat on-ramp correctly is one of the highest-leverage decisions a crypto exchange can make. This guide gives you the numbers, the architecture, and the vendor comparisons to make a confident decision.

💳 What is a Fiat On-Ramp?

A fiat on-ramp allows users to buy crypto using traditional currencies via:

- UPI / Bank transfer

- Debit/Credit cards

- Wallets & payment apps

👉 Example: A user deposits ₹10,000 → instantly buys BTC or USDT.

Why Fiat On-Ramp Integration Is a Revenue-Critical Decision

Fiat on-ramp conversion isn’t a UX problem — it’s a revenue problem. Industry benchmarks put checkout abandonment at the fiat conversion step between 62–70%, higher than nearly any other e-commerce category. Every percentage point you recover compounds directly into trading volume, fee revenue, and user lifetime value.

Choosing the wrong crypto payment integration path — a provider with weak card approval rates in your target market, or a compliance setup that triggers excessive false positives — is one of the fastest ways to stall early growth.

“Your on-ramp is your front door. If the lock is stiff, most people will walk away before they ever see what’s inside.”

This guide covers every major integration approach — hosted widget providers, payment service providers (PSPs), and direct banking APIs — with honest data on fees, approval rates, and compliance overhead.

Who this is for: Crypto exchange founders, fintech product managers, and blockchain developers evaluating build-vs-buy decisions before committing engineering resources.

The Fiat On-Ramp Landscape: Three Integration Approaches

Before comparing specific vendors, it helps to understand the three structural models available for crypto exchange fiat integration.

1. Hosted Widget / White-Label Aggregators

Providers like MoonPay, Transak, Ramp Network, and Banxa operate as fully licensed intermediaries. They handle KYC, AML screening, card processing, and banking relationships on your behalf. You embed their widget with a few lines of JavaScript and receive a webhook when a purchase completes.

- ✅ Low compliance burden on your team

- ✅ Days to integrate, not weeks

- ⚠️ Thinner margins — you’re paying for their licensing and infrastructure

2. Payment Service Providers (PSPs) with Crypto Support

Stripe’s fiat-to-crypto on-ramp sits in the middle ground: developer-grade API control, Stripe’s battle-tested payment infrastructure, and crypto-specific features like wallet address validation and blockchain settlement. Best suited for teams already in the Stripe ecosystem who want native API integration without a fully hosted widget.

3. Direct Banking APIs (ACH, SEPA, Open Banking)

Integrating directly with bank rails — ACH in the US, SEPA Credit Transfer, or Open Banking (PSD2) in Europe — delivers the lowest per-transaction fees, often under 0.5%. The trade-off is significant: you need your own Money Transmitter License (MTL) or a partnership with a licensed entity, plus substantial engineering investment.

⚠️Compliance Note: Direct banking integration without an appropriate MTL or e-money license is illegal in most jurisdictions, including the US, UK, and EU. The licensing timeline runs 6–18 months — plan accordingly.

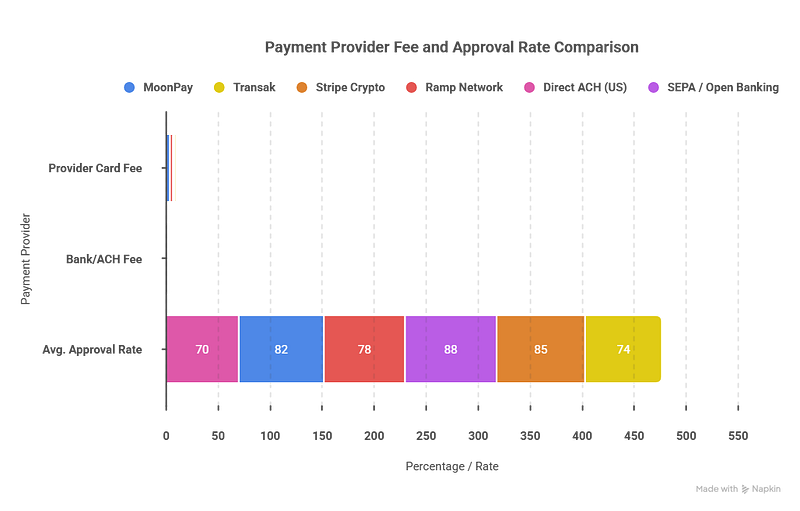

Side-by-Side Comparison: Fees, Approval Rates & Compliance

The table below synthesizes publicly available pricing, documented approval rate benchmarks, and compliance requirements as of Q1 2025. Approval rates vary significantly by geography, card type, and your configured risk thresholds.

Key takeaways:

- Transak offers the lowest card fees among widget providers

- Stripe delivers the best card approval rates with developer-grade control

- Direct SEPA has the highest bank transfer approval rates — but requires EU regulatory standing

Provider Deep-Dives

Stripe Crypto: Best for Developer Teams Already on Stripe

Stripe’s fiat-to-crypto on-ramp handles card acceptance and ACH bank debits with built-in wallet address validation for EVM-compatible chains.

Strengths:

- Industry-leading card approval rates (~85%) driven by Stripe’s issuer relationships and ML-based fraud models

- Radar fraud protection with customizable rules for crypto-specific patterns (velocity, geo-mismatch)

- Familiar API conventions — same developer experience as core Stripe Payments

- Built-in dispute handling and chargeback management

Limitations:

- Geographic coverage is still expanding — limited availability in LATAM and Africa

- KYC is only partially handled; you’ll need your own AML program for regulatory thresholds

- Some issuing banks still decline at the card network level — outside Stripe’s control

// Stripe On-Ramp: minimal integration example

const session = await stripe.crypto.onrampSessions.create({

transaction_details: {

destination_currency: 'eth',

destination_exchange_amount: '0.05',

wallet_address: '0xYourWalletAddress',

},

customer_ip_address: req.ip,

});

// Returns: session.redirect_url — forward user to Stripe-hosted pageMoonPay: Best for Speed to Market and Global Reach

MoonPay is the most widely deployed crypto on-ramp widget by volume, powering integrations for MetaMask, Trust Wallet, and OpenSea. Its edge is breadth: 160+ countries, 30+ fiat currencies, and a licensing portfolio that includes US MSB, UK FCA, and EU VASP registrations.

Approval rates by region:

Region Approval Rate US (Visa/MC) 86% UK / EU 83% SEA / LATAM 71% Africa / MENA 58%

The 4.5% card fee is the highest in the widget category, but MoonPay justifies it with near-zero integration overhead — most partners ship in days. For early-stage exchanges, that time-to-market advantage often outweighs the margin difference.

Pro Tip: MoonPay’s volume-based fee negotiation kicks in at $500K monthly GMV. If you’re approaching that threshold, open the commercial conversation before your renewal window.

Transak: Best for Fee Efficiency and Broad Chain Support

Transak has emerged as MoonPay’s strongest challenger, particularly for exchanges where margin matters. At 1.0–2.5% on card transactions versus MoonPay’s 3.5–4.5%, the fee difference is meaningful for high-frequency retail use cases.

Transak supports 130+ cryptocurrencies and 170+ countries, with coverage across both EVM and non-EVM chains including Solana, Cosmos, and Polkadot. KYC/AML is handled via Jumio and Onfido integrations, with average Tier 1 completion times of 2–4 minutes.

Strengths:

- Lowest card fees in the widget category

- NFT on-ramp support — direct fiat-to-NFT purchase flow (unique in the market)

- Full white-label option for UI customization

- Developer-friendly SDK with React components and deep-link URL configuration

Watch-outs:

- Card approval rates lag MoonPay by ~8% in the US (fewer direct acquirer relationships)

- Enterprise support SLAs have historically been slower than MoonPay

Direct Banking APIs: ACH, SEPA, and Open Banking

Direct bank transfer integration is the path for exchanges operating at scale with maximum margin. Instead of paying a third party 1–4.5% per transaction, you pay the raw ACH or SEPA fee — often under $0.50 per transfer.

ACH in the United States

Via providers like Plaid, Synapse, or direct NACHA membership, ACH debits settle in 1–3 business days. Same-Day ACH reduces this to hours for amounts under $1M.

The non-negotiable requirement: ACH debits for crypto purchases require an MTL in most US states, or a partnership with a licensed MSB. Expect 6–18 months and $50K–$300K in fees and legal costs. A nationwide MTL requires approval in up to 49 states.

SEPA and Open Banking in Europe

PSD2 enables payment initiation directly from user bank accounts with strong customer authentication (SCA). Providers like TrueLayer, Yapily, and Tink aggregate Open Banking APIs across 30+ European markets, with same-day or T+1 settlement.

Operating as a Payment Initiation Service Provider (PISP) requires registration as a Payment Institution (PI) or Electronic Money Institution (EMI). The FCA (UK), BaFin (Germany), and DNB (Netherlands) are common first-license targets.

MiCA Note: The EU’s MiCA regulation (fully applicable from December 2024) adds a Crypto Asset Service Provider (CASP) registration layer on topof existing PSD2 licensing. Map both frameworks with compliance counsel before building.

Compliance Architecture: KYC, AML, and Licensing

Crypto exchange KYC compliance is the single biggest variable in on-ramp integration timelines. Your payment path largely determines your compliance architecture.

Using a Hosted Widget Provider

The provider holds the VASP/MSB/MTL licenses and performs KYC on your behalf. You receive a pseudonymous user ID and completion status. This is legally cleaner for early-stage exchanges but creates a data separation problem — your KYC records and the provider’s aren’t linked unless you build an explicit integration.

Building Your Own AML Program

For direct banking or Stripe integrations, your minimum viable AML program needs:

- Identity Verification (IDV): Jumio, Onfido, or Persona for document + liveness checks

- Sanctions Screening: Chainalysis, Elliptic, or TRM Labs for wallet screening; Dow Jones / LexisNexis for name screening

- Transaction Monitoring: Rule-based alerts (velocity, structuring) plus ML-based anomaly detection

- SAR Filing: Automated suspicious activity report workflows (US: FinCEN; UK: NCA)

- Travel Rule Compliance: IVMS101 data exchange for transfers above $3K (US) / €1K (EU)

Tiered KYC Structure

Tier Requirements Daily Limit Conversion Rate Impact Tier 0 Email + wallet $150–$250 Highest Tier 1 Gov ID + selfie $5,000–$15,000 Medium drop Tier 2 Proof of address + source of funds $50,000+ Significant drop

Integration Architecture and Code Patterns

Regardless of which provider you choose, these engineering patterns apply universally.

Webhook-Driven State Management

Never confirm payment completion via client-side redirects. Card authorizations can reverse, ACH transfers can return, and bank-side failures can occur after the user has already left your UI. Build your order state machine around provider webhooks.

// Webhook handler pattern (Node.js / Express)

app.post('/webhooks/onramp', express.raw({type: 'application/json'}), (req, res) => {

const event = verifyWebhook(req.body, req.headers['x-signature']); switch(event.type) {

case 'payment.completed':

await updateOrderStatus(event.data.orderId, 'CONFIRMED');

await triggerCryptoRelease(event.data.walletAddress, event.data.amount);

break;

case 'payment.failed':

await updateOrderStatus(event.data.orderId, 'FAILED');

await notifyUser(event.data.userId, 'PAYMENT_FAILED');

break;

}

res.sendStatus(200);

});Multi-Provider Fallback Routing

If your primary provider declines a transaction, automatically retry through a secondary provider. In lower-approval markets like LATAM, MENA, and Southeast Asia, approval rate variance between providers can exceed 20 percentage points. This single architectural decision can meaningfully lift your overall conversion rate.

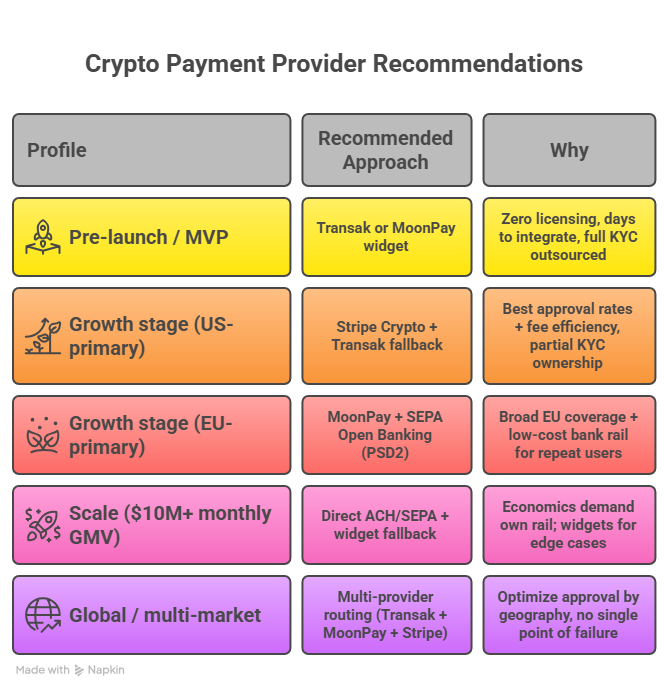

Which On-Ramp Should You Choose?

The right answer depends on your current stage, target market, and compliance resources:

Frequently Asked Questions

What is the cheapest fiat on-ramp for a crypto exchange?

For bank transfers, direct SEPA is the lowest cost at €0.10–€0.25 flat per transaction, but requires an EU Payment Institution license. Among hosted widgets, Transak offers the lowest card fees at 1.0–2.5%. At $10M+ monthly GMV, direct ACH typically wins on economics once licensing is secured.

Does Stripe support crypto exchange integration in 2026?

Yes. Stripe’s crypto on-ramp supports fiat-to-crypto purchases via card and ACH for US users, with developer-grade API access and ~85% card approval rates. Geographic availability is expanding — verify current country support in Stripe’s documentation before building.

Do I need a money transmitter license to use MoonPay or Transak?

No. Both operate as licensed intermediaries and you use their licenses. Their fees are higher precisely because of this. Have legal counsel review your specific business model regardless, as the regulatory picture depends on your structure and user geography.

What causes low card approval rates on crypto purchases?

Three factors: issuing banks apply categorical declines for crypto merchants; card network rules restrict certain card types; and fraud models flag the new-user-plus-crypto pattern as high risk. Fix it by choosing providers with direct issuer relationships, implementing 3DS2, and segmenting retry logic by card type and geography.

Can I use multiple on-ramp providers simultaneously?

Yes — and for production exchanges, it’s strongly recommended. A multi-provider routing architecture can increase overall approval rates by 10–15 percentage points versus single-provider deployments. The engineering overhead is real, but the revenue impact at scale justifies it.

What’s the difference between MoonPay and Transak?

MoonPay has stronger brand recognition, slightly better approval rates in Tier 1 markets, and more mature enterprise support. Transak offers meaningfully lower fees, broader cryptocurrency support, and NFT on-ramp capabilities. For most early-stage exchanges: start with Transak, add MoonPay as a fallback once volume warrants it.

📞 Get a Free Consultation Today!

Get More Information: + 91- 452 498 7177, +91–9003028042

Website — https://shorturl.at/Zcz7L

Email us -business@spiegeltechnologies.com

𝐓𝐞𝐥𝐞𝐠𝐫𝐚𝐦 -> https://t.me/SpiegelTech

𝐖𝐡𝐚𝐭𝐬𝐀𝐩𝐩 ->91–9003028042

Comments